.png)

.png)

Symptoms For ABCM Analysis

.png)

.png)

Value Addition with an ABCM Assignment

• A significant/improved focus on customer-centric activities and value-added focus for all activities and depts.

• Involvement of all HODs in working capital management and cost ownership with enhanced action plans and motivation.

• Elimination / Reduction of non-value-added activities and quantified agenda for all personnel and departments.

Serious multiple caps for people, fully owned up additional KRAs, and eliminating the demotivating cross-subsidies that exist.

• More motivating performance management reviews for people and product groups, geographies, branches, Sectors, and applications.

• Numerical Evolution of personnel at all levels to discuss and talk in quantified terms rather than being vague.

Significant Cross-functional, well-knit working teams and wiping out the Silo approach of stubborn archaic working methods.

• Quantified approach to daily life and ensuring people are specific and to the point in all discussions and behaviour.

• Understanding the unabsorbed costs of the organization which are not Product/Service costs and are actually the quantified slack.

• Interplant comparisons for performance reviews and Benchmarking.

• Improved Throughput, Profitability, and Employee Motivation.

• Idle capacity is isolated and not charged to a product or service. Under traditional approaches, some idle capacity may be incorporated into the overhead allocation rates, thereby potentially distorting the cost of specific output. This may limit the ability of managers to truly understand and identify the best business decisions about product pricing and targeted production levels.

• Improves Management’s focus on the firm’s critical success factors thereby enhancing the firm’s competitive advantage.

Managers

.png)

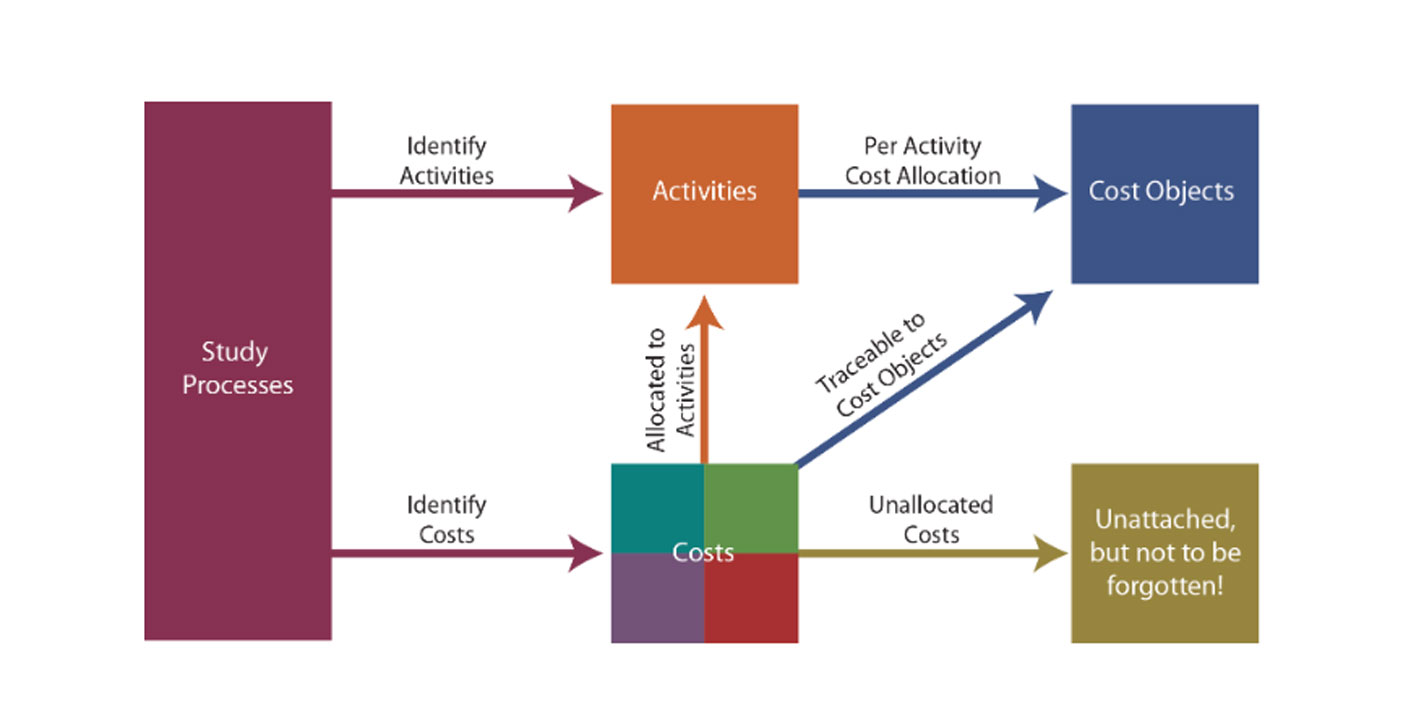

Methodology

.png)

For Strategic Decision-making

.png)

.png)

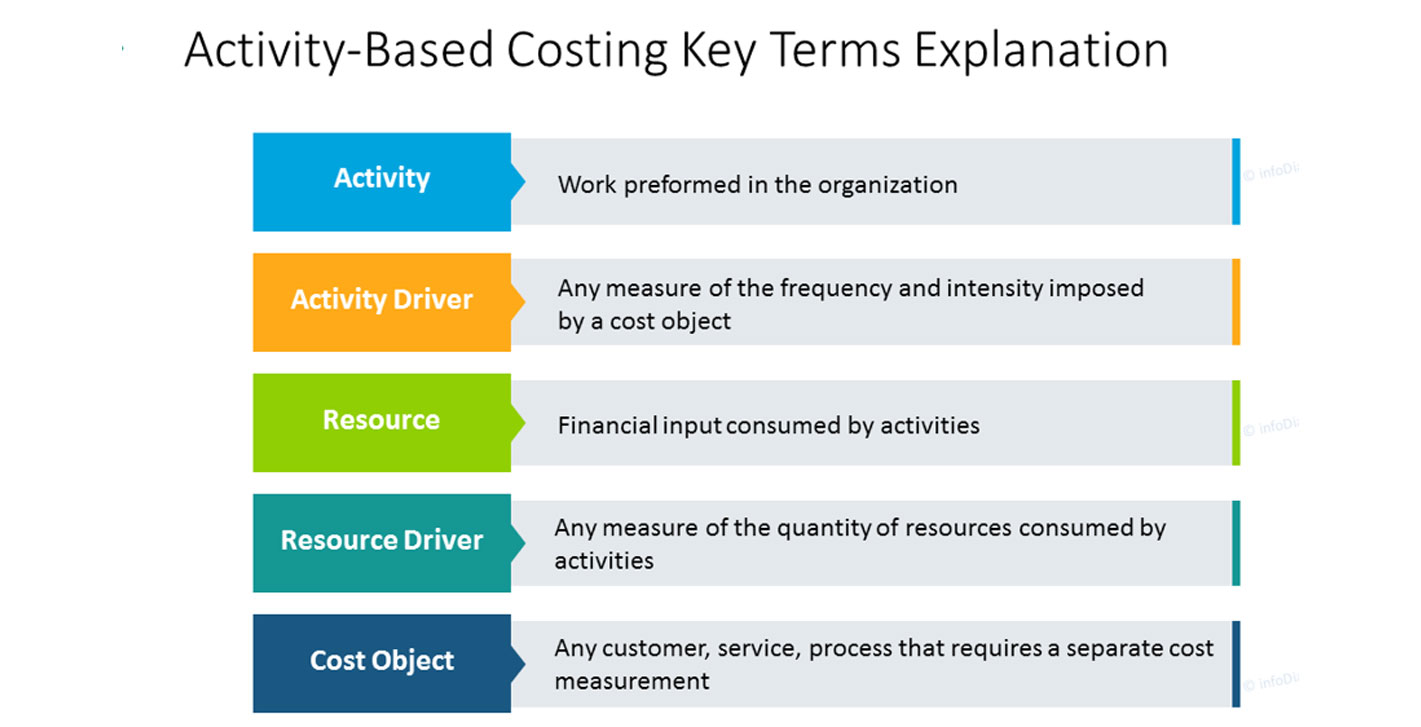

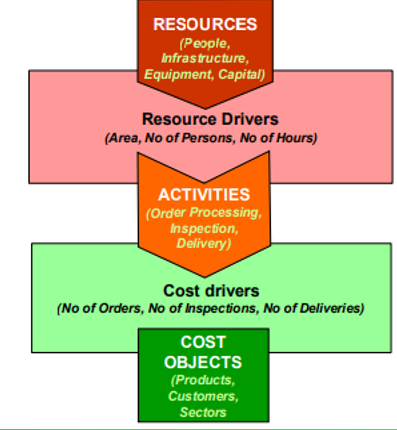

Why are Activities so Important for Analysis

Why ABCM is so popular for improved performance & planning

.png)

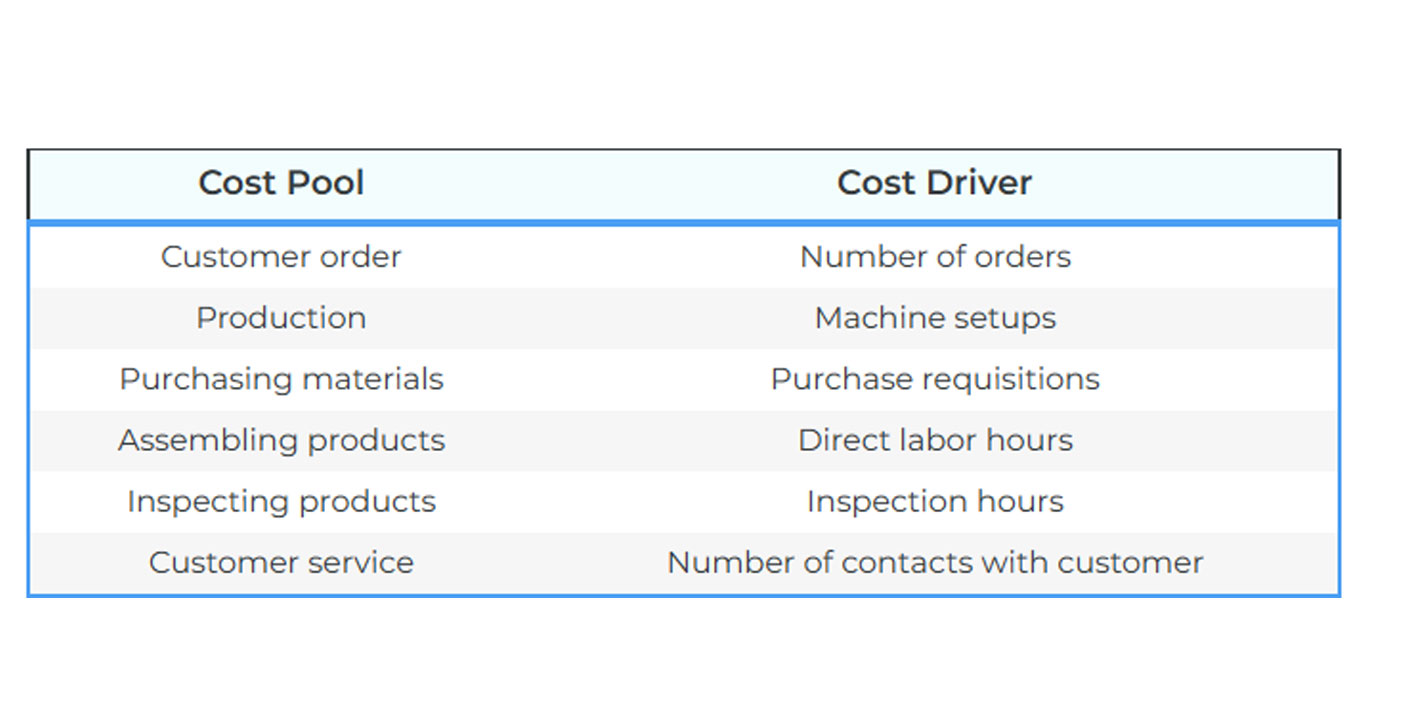

Some Example

.png)

.png)

.png)

.png)

.png)

.png)